The cross-correlation function (CCF) helps you determine which lags of time series X predicts the value of time series Y. However, if either series contain autocorrelation, or the two series share common trends, it is difficult to identify meaningful relationships between the two time series. Pre-whitening solves this problem by removing the autocorrelation and trends.

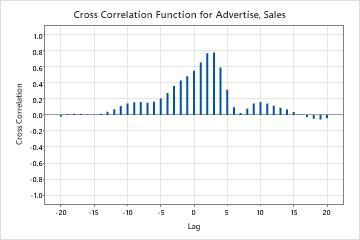

This cross-correlation function shows large correlations at lags 2 and 3 with the correlations on both sides slowly decreasing to 0. This pattern indicates that you may need to pre-whiten your data to help you understand the relationship between the two time series.

There are different methods for pre-whitening data. Complete the following steps to pre-whiten your data using one variety of the equal footing method.

- For one of your variables, perform one of the following smoothing analyses.

To determine the appropriate analysis, go to Which time series analysis should I use?

- Store the residuals from the smoothing analysis that you selected.

- Go to , and enter the column of stored residuals in Series.

- Under Nonseasonal, in Autoregressive enter 5.

- Deselect Include constant term in model.

- Select Storage and select Residuals.

- Click OK in each dialog.

- Repeat steps 1-7 for your other variable.

- Verify that both time series have been reduced to white noise. Your data has been reduced to white noise when there are no trends, patterns, or autocorrelation. To verify this, you can use a time series plot and autocorrelation.

- Perform a cross-correlation analysis using the two columns of stored residuals from the ARIMA analyses.