Select the method or formula of your choice.

ACF

The graphs for the autocorrelation function (ACF) of the ARIMA residuals include lines that represent the significance limits. Values that extend beyond the significance limits are statistically significant at approximately α = 0.05, and show evidence that the autocorrelation does not equal zero.

Formula

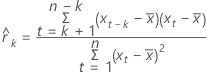

Notation

| Term | Description |

|---|---|

| k | lag; k = 1, 2,... |

| xt | value of x at row t |

| mean of x |

| n | number of observations in the series |

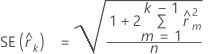

Standard error of ACF

Formula

Notation

| Term | Description |

|---|---|

|  |

| k | lag; k = 1, 2, ... |

| n | number of observations in the series |

| autocorrelation of lag m |

t-statistics

Formula

Notation

| Term | Description |

|---|---|

| autocorrelation at lag k; k = 1, 2, ... |

| standard error of the autocorrelation at lag k |

Significance limits

Formula

Upper limit at lag k = t n−1; 0.975 × SE(rk )

Lower limit at lag k = t n−1; 0.025 × SE(rk )

Notation

| Term | Description |

|---|---|

| SE(rk ) | standard error of the autocorrelation at lag k |

| t n-1; 0.975 | 97.5th percentile of the t distribution with n – 1 degrees of freedom |

| t n-1; 0.025 | 2.5th percentile of the t distribution with n – 1 degrees of freedom |

Ljung-Box Q statistic

Formula

Notation

| Term | Description |

|---|---|

| n | number of observations in a series |

| estimated autocorrelation at lag m; m = 1, 2, ..., k |

| k | lag; k = 1, 2, ... |